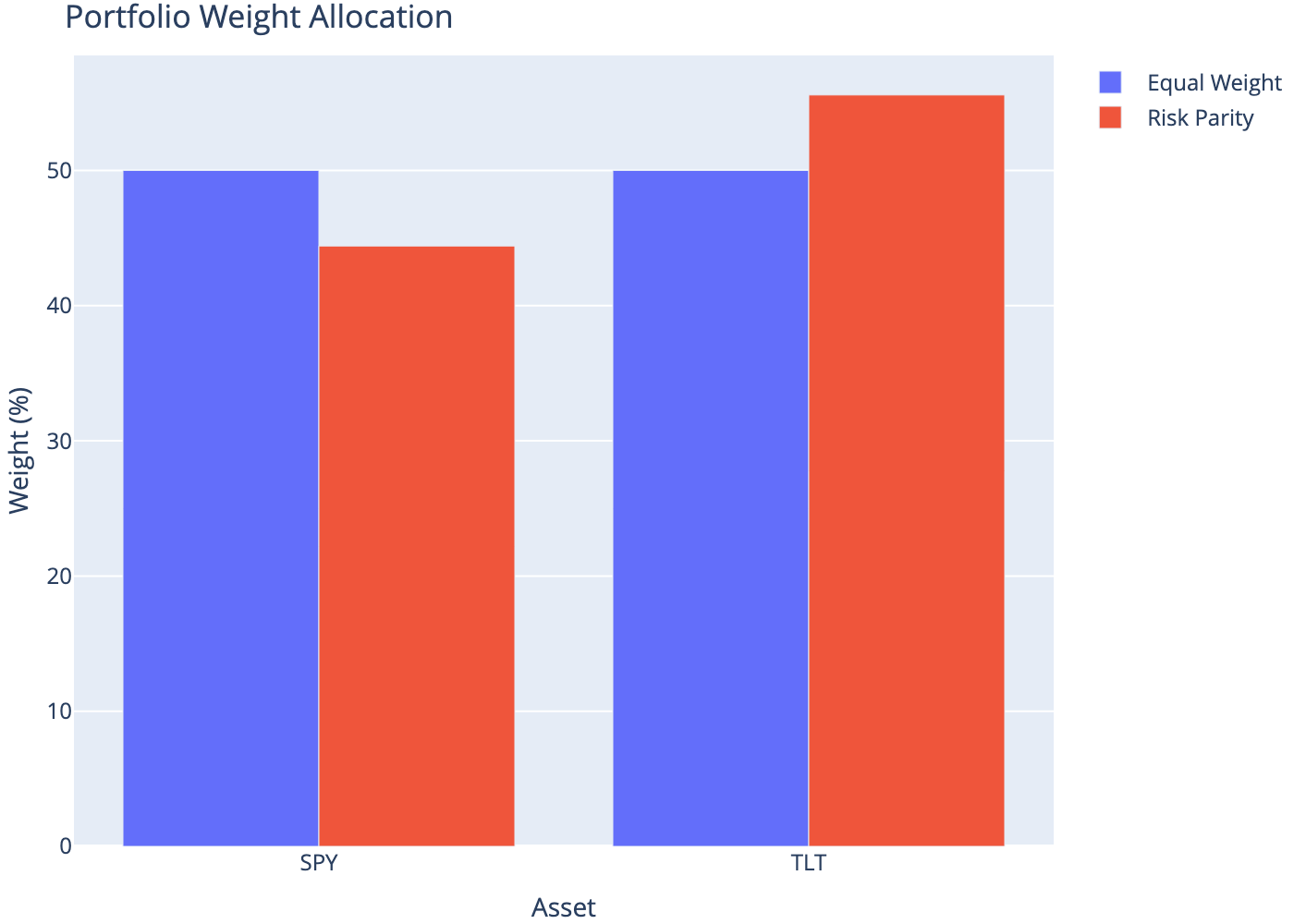

| Ticker | Ann. Volatility (%) | Risk Parity Weight (%) | |

|---|---|---|---|

| Ticker | |||

| SPY | SPY | 16.27 | 44.41 |

| TLT | TLT | 13.00 | 55.59 |

Risk Parity

Portfolio allocation based on equal risk contribution

finance

basics

portfolio

An introduction to risk parity, a strategy that allocates capital inversely proportional to asset volatility.

1 Abstract

Risk Parity is a portfolio allocation strategy where each asset contributes equally to the total portfolio risk. Unlike equal-weight portfolios (where each asset receives equal capital), risk parity allocates less capital to high-volatility assets and more capital to low-volatility assets. This approach was popularized by Bridgewater Associates’ “All Weather” fund and formalized by Qian (2005).

2 Definitions

Consider a portfolio of \(n\) assets with weights \(w_i\) where \(\sum_{i=1}^{n} w_i = 1\).

For the simplified case (assuming uncorrelated assets), the inverse volatility weighting formula is:

\[ w_i = \frac{\frac{1}{\sigma_i}}{\sum_{j=1}^{n} \frac{1}{\sigma_j}} \]

Where \(\sigma_i\) is the standard deviation (volatility) of asset \(i\).

For a two-asset portfolio (assets A and B):

\[ w_A = \frac{\frac{1}{\sigma_A}}{\frac{1}{\sigma_A} + \frac{1}{\sigma_B}} = \frac{\sigma_B}{\sigma_A + \sigma_B} \]

\[ w_B = \frac{\frac{1}{\sigma_B}}{\frac{1}{\sigma_A} + \frac{1}{\sigma_B}} = \frac{\sigma_A}{\sigma_A + \sigma_B} \]

Note: This simplification assumes zero correlation between assets. For correlated assets, the full covariance matrix must be considered (Maillard et al., 2010).

3 Theoretical Example

Given two assets with annualized volatilities:

- Asset A: \(\sigma_A = 4.50\%\)

- Asset B: \(\sigma_B = 1.62\%\)

Applying the inverse volatility formula:

\[ w_A = \frac{1.62}{4.50 + 1.62} = \frac{1.62}{6.12} \approx 26.47\% \]

\[ w_B = \frac{4.50}{4.50 + 1.62} = \frac{4.50}{6.12} \approx 73.53\% \]

The higher-volatility asset (A) receives less capital, while the lower-volatility asset (B) receives more.

4 Compute (Python)

We apply risk parity to a classic stock-bond portfolio using SPY (S&P 500 ETF) and TLT (20+ Year Treasury Bond ETF).

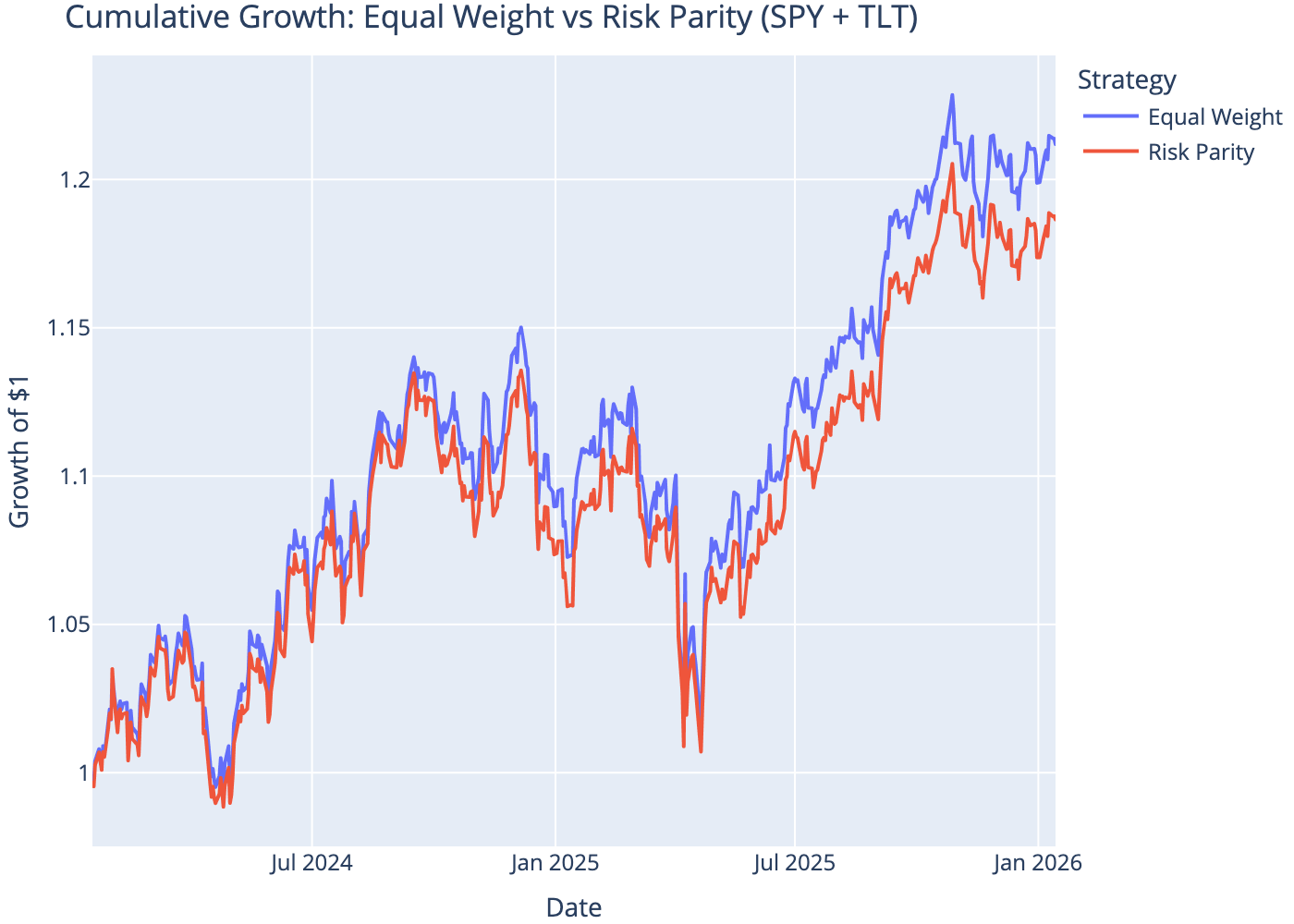

5 Comparison: Equal Weight vs Risk Parity

| Portfolio | Ann. Return (%) | Ann. Volatility (%) | Sharpe Ratio | |

|---|---|---|---|---|

| 0 | Equal Weight | 10.25 | 10.78 | 0.95 |

| 1 | Risk Parity | 9.16 | 10.59 | 0.87 |

6 Portfolio Performance

7 Weight Allocation

8 Conclusion

Risk parity allocates capital inversely proportional to volatility, ensuring each asset contributes similar risk to the portfolio. In a stock-bond portfolio, this typically results in overweighting bonds (lower volatility) relative to stocks (higher volatility). This approach often achieves lower portfolio volatility and improved risk-adjusted returns compared to equal-weight allocations.

References

Maillard, S., Roncalli, T., & Teïletche, J. (2010). The properties of equally weighted risk contribution portfolios. Journal of Portfolio Management, 36(4), 60–70.

Qian, E. (2005). Risk parity portfolios: Efficient portfolios through true diversification. Panagora Asset Management.