Initial Price: $689.42

Annual Drift (μ): 19.97%

Annual Volatility (σ): 16.26%Geometric Brownian Motion

Stochastic modeling of asset prices

finance

basics

stochastic

An introduction to Geometric Brownian Motion (GBM), the foundation of modern option pricing and Monte Carlo simulation.

1 Abstract

Geometric Brownian Motion (GBM) is a continuous-time stochastic process used to model stock prices. It forms the foundation of the Black-Scholes option pricing model and assumes that prices follow a random walk consistent with the weak-form efficient market hypothesis.

2 Definition

The stochastic differential equation (SDE) for GBM is:

\[ dS = \mu S \, dt + \sigma S \, dW \]

Where:

- \(S\) = asset price

- \(\mu\) = drift (expected return)

- \(\sigma\) = volatility (standard deviation of returns)

- \(dW\) = Wiener process (standard Brownian motion)

3 Discrete Form

For simulation purposes, we use the discrete approximation:

\[ \frac{\Delta S}{S} = \mu \Delta t + \sigma \varepsilon \sqrt{\Delta t} \]

Where \(\varepsilon \sim N(0,1)\) is a standard normal random variable.

The first term (\(\mu \Delta t\)) is the drift — the expected directional movement. The second term (\(\sigma \varepsilon \sqrt{\Delta t}\)) is the shock — random fluctuation scaled by volatility.

4 Analytical Solution

The exact solution to the GBM SDE is:

\[ S(t) = S_0 \exp\left[\left(\mu - \frac{\sigma^2}{2}\right)t + \sigma W(t)\right] \]

This shows that prices are log-normally distributed (always positive), while returns are normally distributed.

5 Simulation (Python)

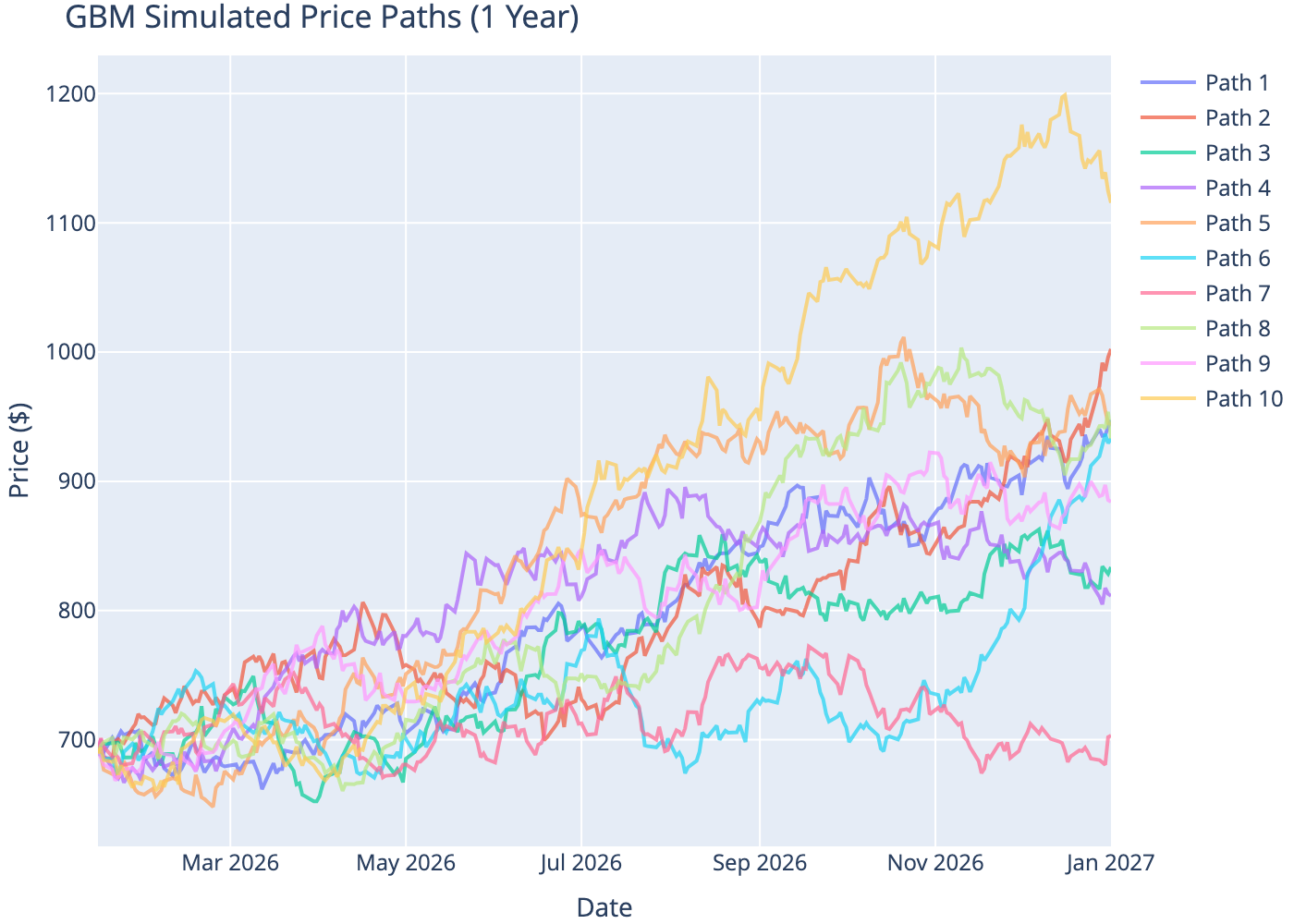

We simulate 10 possible price paths for a stock over 1 year using historical SPY parameters.

| Path 1 | Path 2 | Path 3 | Path 4 | Path 5 | Path 6 | Path 7 | Path 8 | Path 9 | Path 10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2026-12-28 | 940.351636 | 973.706233 | 816.717561 | 810.539100 | 971.258809 | 919.331363 | 684.347186 | 942.733507 | 888.400176 | 1155.844317 |

| 2026-12-29 | 935.224328 | 991.745409 | 834.179546 | 804.792609 | 966.520387 | 928.150647 | 682.142788 | 942.992669 | 889.289266 | 1134.171455 |

| 2026-12-30 | 935.784102 | 985.490683 | 830.590012 | 817.389824 | 954.863551 | 936.609321 | 680.699478 | 940.989754 | 897.183859 | 1138.972658 |

| 2026-12-31 | 941.968091 | 996.052310 | 828.388203 | 812.879866 | 945.004999 | 929.409366 | 702.101015 | 953.772625 | 885.504854 | 1124.475841 |

| 2027-01-01 | 947.331151 | 1002.394747 | 833.676855 | 811.359486 | 944.489876 | 933.227374 | 703.239482 | 933.020007 | 884.076480 | 1115.534543 |

6 Simulated Price Paths

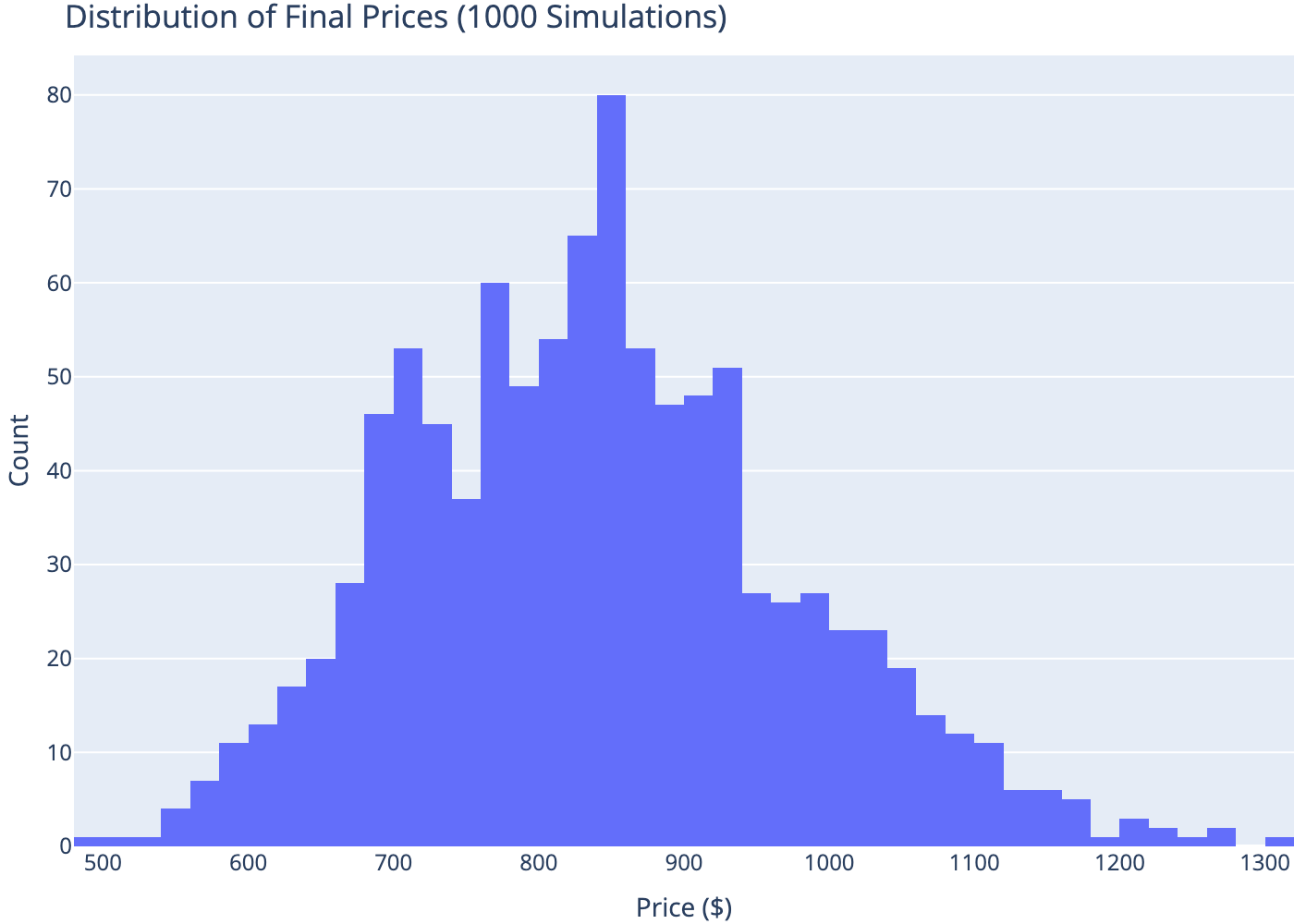

7 Distribution of Final Prices

8 Conclusion

Geometric Brownian Motion provides a mathematically tractable model for asset prices. While it has limitations (assumes constant volatility and continuous trading), GBM remains fundamental to quantitative finance for option pricing, risk management, and Monte Carlo simulation.