Abstract

In random sampling, each member of a population has an equal chance or probability of being selected. This process provides an unbiased representation of the total population where each observation is selected independently.

Definition

Given a population of \(N\) observations, random sampling selects \(n\) observations where each has equal probability:

\[

P(\text{selection}) = \frac{1}{N}

\]

The sample mean \(\bar{x}\) estimates the population mean \(\mu\):

\[

\bar{x} = \frac{1}{n} \sum_{i=1}^{n} x_i

\]

Why Random Sampling?

- Reduces bias: Every data point has equal chance of selection

- Computational efficiency: Analyze subset instead of full dataset

- Statistical validity: Sample statistics approximate population parameters

- Backtesting: Test strategies on random subsets to avoid overfitting

Example (Python)

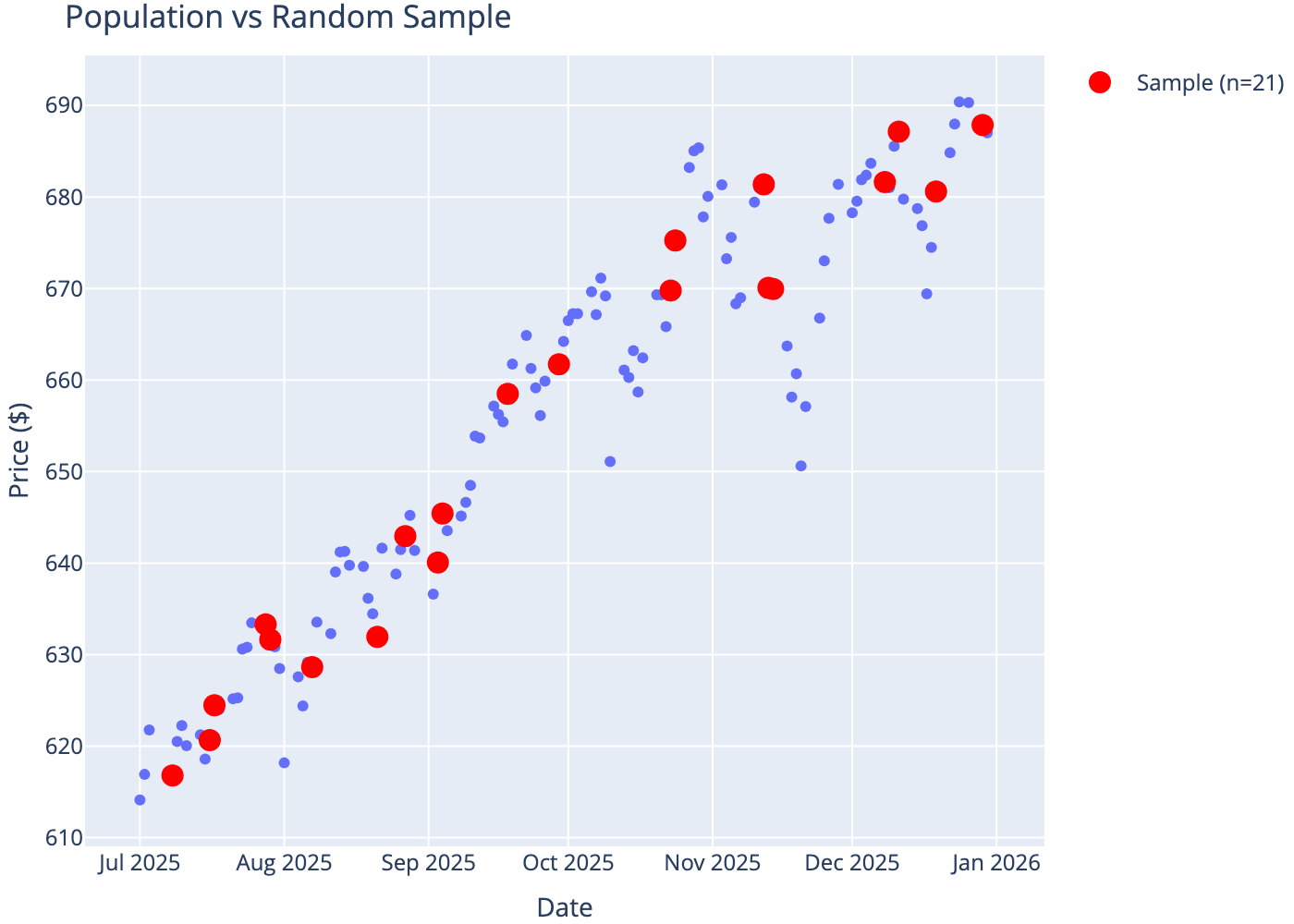

We randomly sample 21 trading days from 6 months of SPY price data.

Population: 127 trading days

Sample: 21 randomly selected days

| 0 |

2025-07-08 |

616.80 |

| 1 |

2025-07-16 |

620.66 |

| 2 |

2025-07-17 |

624.46 |

| 3 |

2025-07-28 |

633.31 |

| 4 |

2025-07-29 |

631.64 |

| 5 |

2025-08-07 |

628.64 |

| 6 |

2025-08-21 |

631.93 |

| 7 |

2025-08-27 |

642.94 |

| 8 |

2025-09-03 |

640.07 |

| 9 |

2025-09-04 |

645.42 |

| 10 |

2025-09-18 |

658.48 |

| 11 |

2025-09-29 |

661.72 |

| 12 |

2025-10-23 |

669.78 |

| 13 |

2025-10-24 |

675.25 |

| 14 |

2025-11-12 |

681.37 |

| 15 |

2025-11-13 |

670.06 |

| 16 |

2025-11-14 |

669.95 |

| 17 |

2025-12-08 |

681.62 |

| 18 |

2025-12-11 |

687.14 |

| 19 |

2025-12-19 |

680.59 |

| 20 |

2025-12-29 |

687.85 |

Sample vs Population

| 0 |

Mean Price |

655.67 |

654.27 |

| 1 |

Std Dev |

21.95 |

24.05 |

| 2 |

Min |

614.13 |

616.80 |

| 3 |

Max |

690.38 |

687.85 |

Conclusion

Random sampling enables unbiased analysis of large datasets using smaller representative subsets. The sample statistics approximate the population parameters, making it a fundamental technique in quantitative finance for backtesting and model validation.