Stock Price (S): $100

Strike Price (K): $100

Time to Expiration: 3 months

Risk-Free Rate: 5.0%

Volatility: 20.0%

Call Price: $4.61

Put Price: $3.37Black-Scholes Model

Option pricing fundamentals

finance

derivatives

options

The Black-Scholes model provides closed-form solutions for European option prices, revolutionizing derivatives pricing.

1 Abstract

The Black-Scholes model, published by Fischer Black and Myron Scholes in 1973, provides a closed-form solution for pricing European-style options (Black & Scholes, 1973). The model assumes geometric Brownian motion for the underlying asset and derives option prices through a no-arbitrage argument. Despite its simplifying assumptions, Black-Scholes remains the foundation of options pricing and risk management.

2 Assumptions

The Black-Scholes model assumes:

- Stock price follows geometric Brownian motion with constant \(\mu\) and \(\sigma\)

- Risk-free rate \(r\) is constant

- No dividends during the option’s life

- European-style exercise (only at expiration)

- No transaction costs or taxes

- Continuous trading is possible

- No arbitrage opportunities exist

3 The Black-Scholes Formula

Call option price: \[ C = S_0 N(d_1) - K e^{-rT} N(d_2) \]

Put option price: \[ P = K e^{-rT} N(-d_2) - S_0 N(-d_1) \]

Where: \[ d_1 = \frac{\ln(S_0/K) + (r + \sigma^2/2)T}{\sigma\sqrt{T}} \]

\[ d_2 = d_1 - \sigma\sqrt{T} \]

- \(S_0\) = current stock price

- \(K\) = strike price

- \(T\) = time to expiration (years)

- \(r\) = risk-free rate

- \(\sigma\) = volatility

- \(N(\cdot)\) = cumulative normal distribution function

4 Compute (Python)

5 Put-Call Parity

A fundamental relationship links call and put prices:

\[ C - P = S_0 - K e^{-rT} \]

C - P = $1.2422

S - Ke^(-rT) = $1.2422

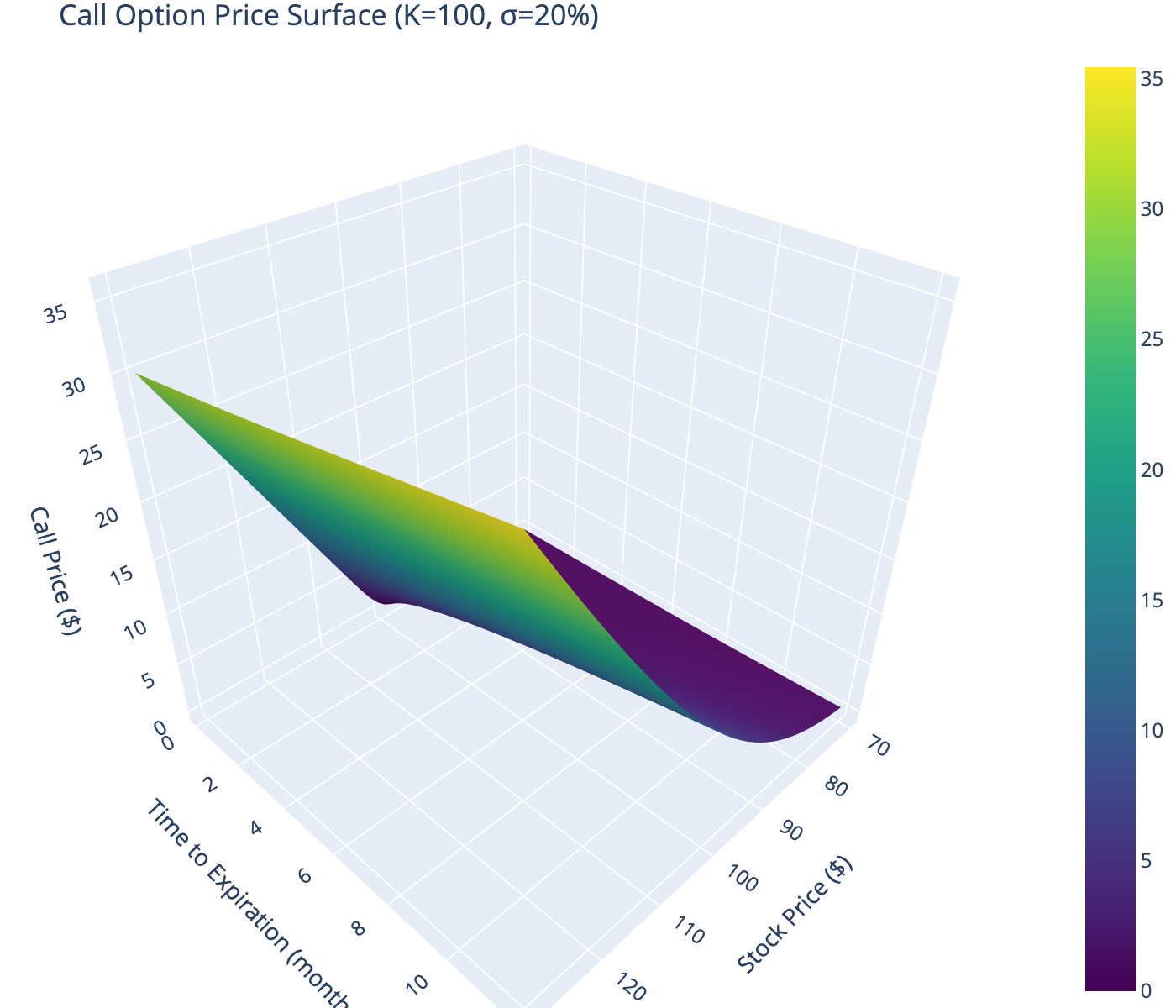

Difference: $0.0000006 Option Price Surface

Option prices vary with stock price and time to expiration.

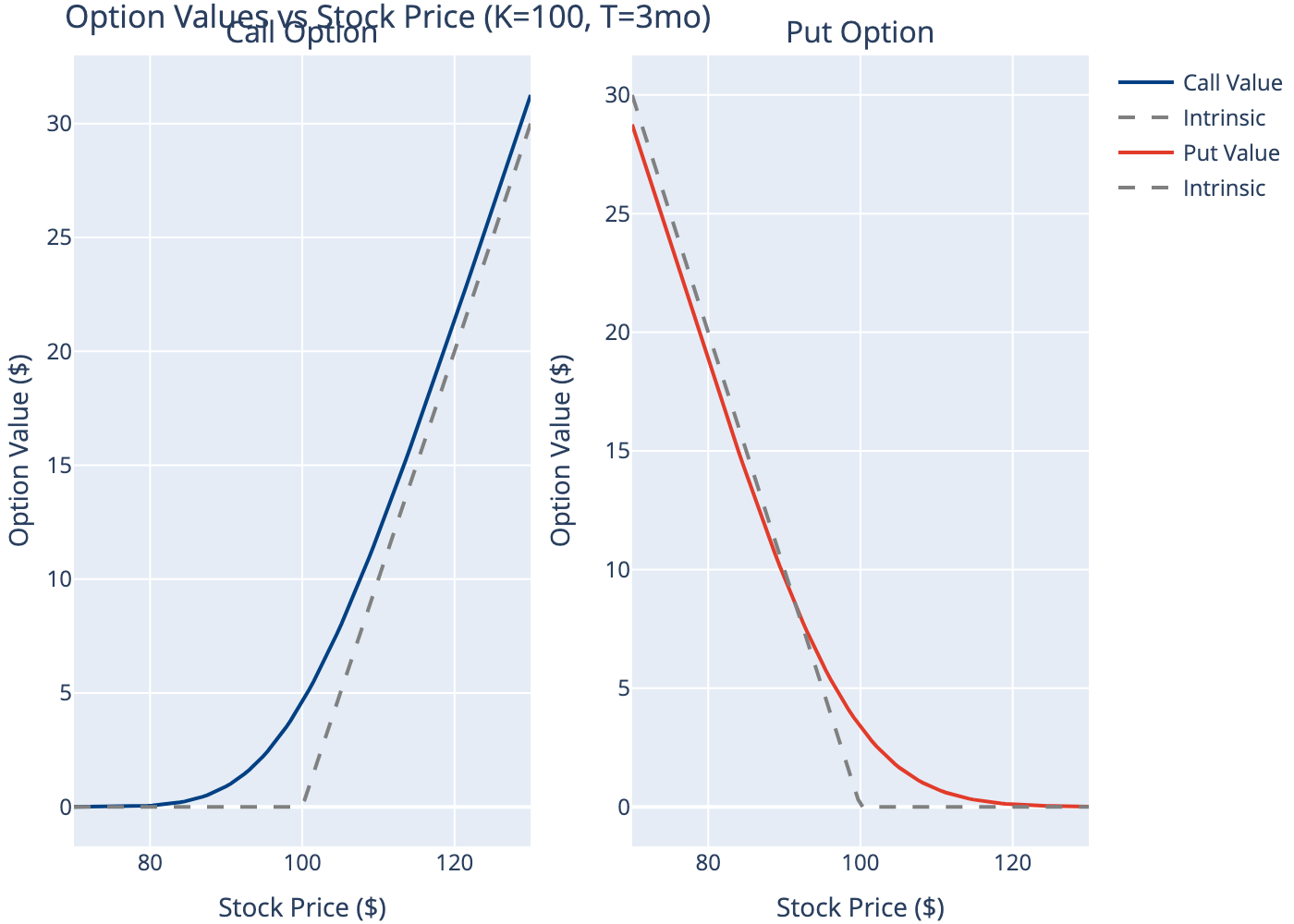

7 Price vs Stock Price

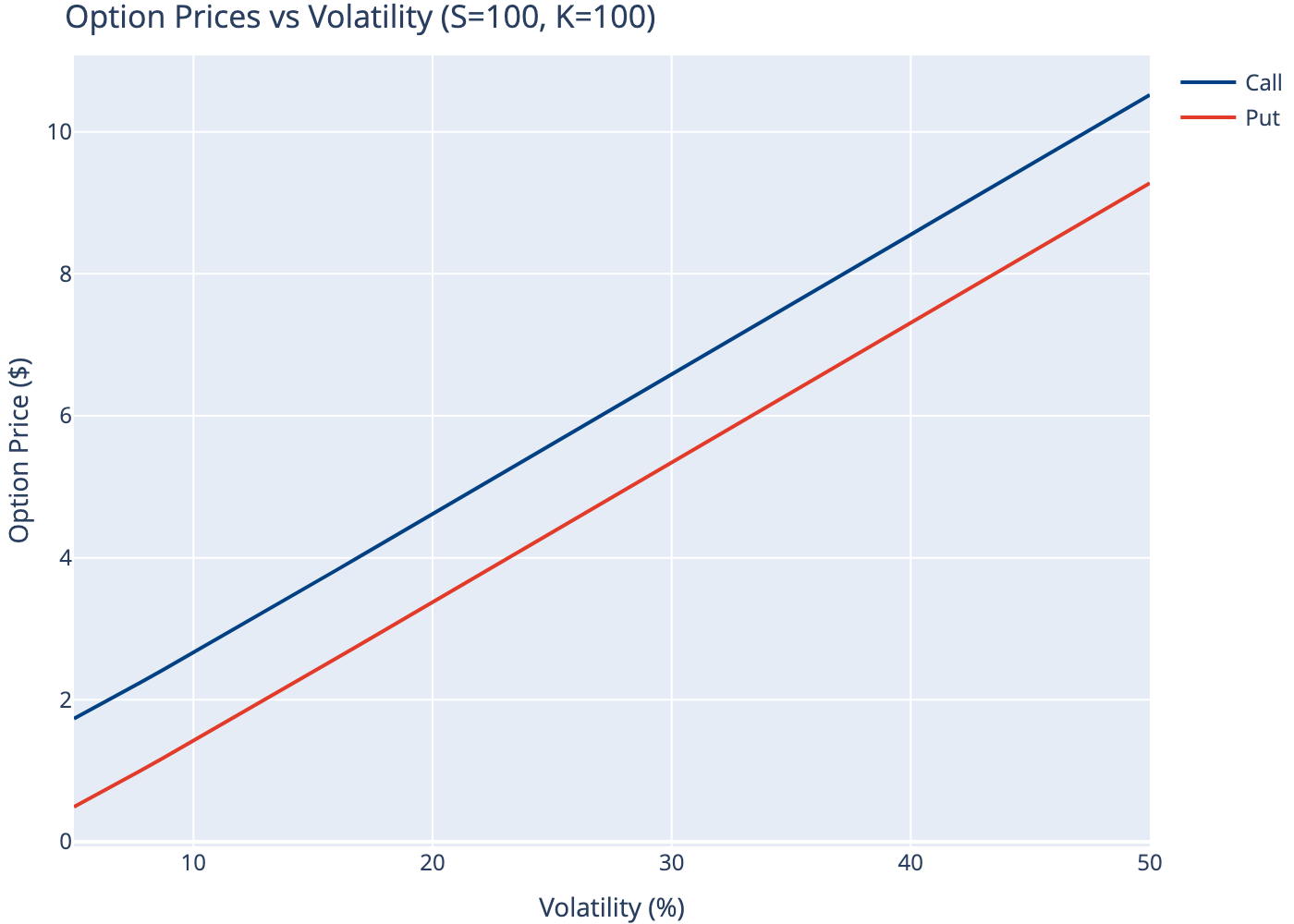

8 Sensitivity to Parameters

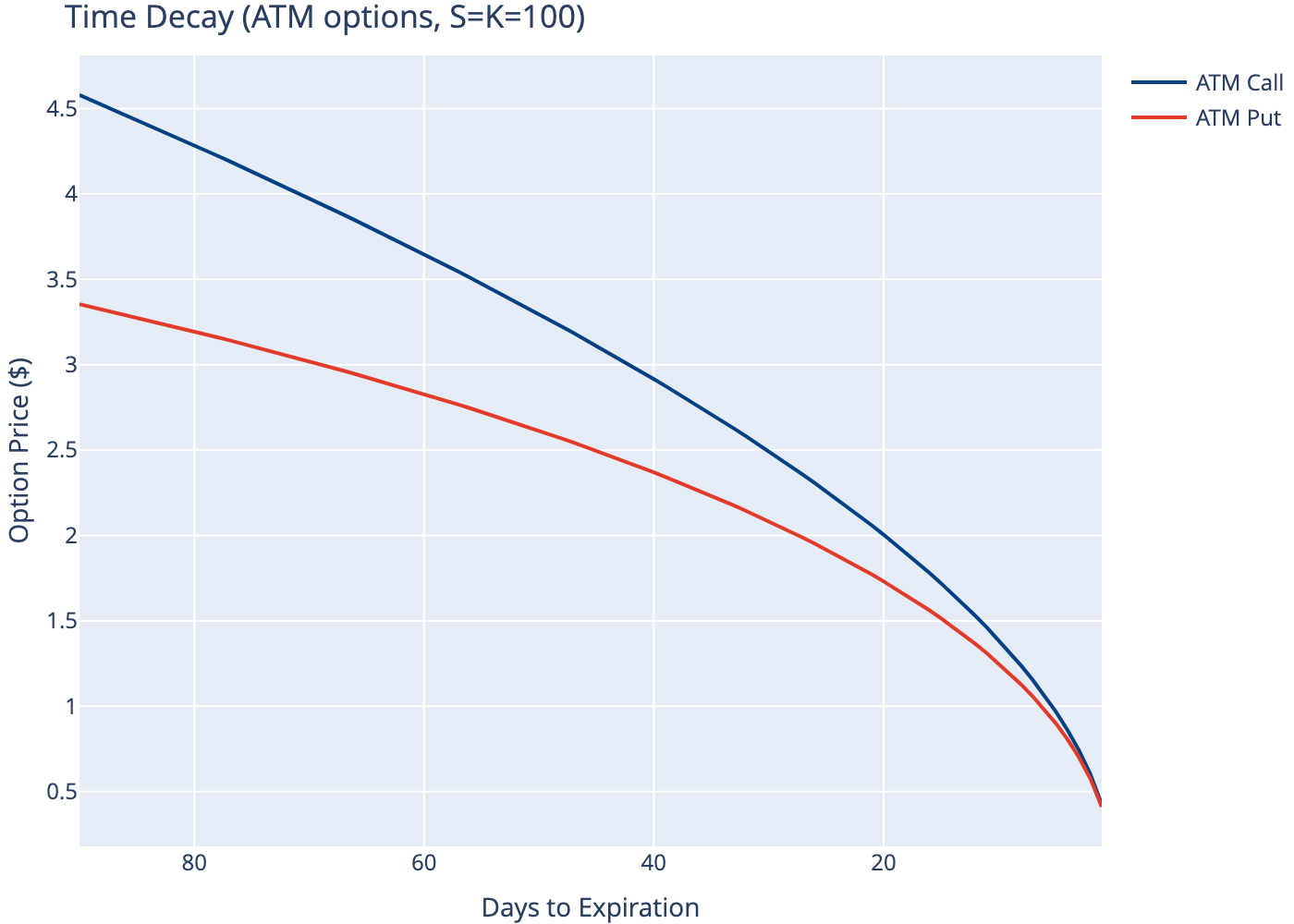

9 Time Decay

10 Option Pricing Table

| Days | 30 | 60 | 90 | 180 |

|---|---|---|---|---|

| Strike | ||||

| 90 | 10.43 | 11.02 | 11.64 | 13.45 |

| 95 | 5.88 | 6.84 | 7.68 | 9.82 |

| 100 | 2.49 | 3.65 | 4.58 | 6.83 |

| 105 | 0.73 | 1.64 | 2.45 | 4.53 |

| 110 | 0.14 | 0.61 | 1.17 | 2.86 |

11 Limitations

- Constant volatility: Real volatility changes over time and varies by strike (volatility smile)

- No dividends: Requires adjustment for dividend-paying stocks

- European only: Cannot price American options with early exercise

- Log-normal prices: Underestimates probability of extreme moves

- Continuous trading: Markets have discrete trading and gaps

Despite these limitations, Black-Scholes provides essential intuition for options pricing and serves as a benchmark for more sophisticated models.

12 Conclusion

The Black-Scholes model revolutionized derivatives pricing by providing a closed-form solution for European options. Understanding its components—the relationship between underlying price, strike, time, volatility, and interest rates—is fundamental to options trading and risk management. While modern practitioners use more sophisticated models, Black-Scholes remains the starting point for options education and a benchmark for model comparison.

References

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637–654.